We’ve all heard about credit cards that give you miles, cash back, and/or any number of benefits for simply using them. The tricky part about credit cards is their ease of use and how quickly the balance on the card can grow out of control. The following is a way to maximize the power of the credit card without crossing over to the dark side of credit card debt.

“Write a check. Record it in your digital tracker. Watch the tracker’s running balance go down. Now, instead of a check, use your credit card. Only this time, don’t use the card beyond what you have in your checking account.”

me, the creator of the digital tracker and planner

It’s easy to say, “Use your credit card like a check.” To do this, however, you need a tool that tracks your spending and allows you to payoff the credit card before it accrues interest.

In my Financial Headaches: A Series on Personal Finance Management, I shared different approaches to the same technique, each based on paycheck timing. The front loaded approach presented in Lesson 5d, which was

- Updated in Lesson 6: Tracking Actual Commitments,

- Balanced in Lesson 7. Balancing Against the Bank, and

- Adjusted in Lesson 8. Adjusting for the Future,

is the approach that will allow you to implement the check-to-credit card switch. Figure 2 below illustrates an example of the front load approach to managing your checking account and personal finances. Notice how January’s paychecks are inline to pay for commitments accrued in February. And February’s paychecks are inline to pay March’s commitments.

The important part about this approach is the ability to stack a group of commitments together. In this case, five weeks of cash card transfers are organized at the end of the month versus in chronological order.

Why do this? Two reasons.

- The required commitments have first dibs on your paycheck, expenses such as rent, loans, utilities.

- The cash card commitments are for expenses, for the most part, you can control. (e.g., how many Iced Cappuccinos you buy or if you need that seventh pair of shoes).

The extra benefit to grouping the cash card commitments last is the ease in which you can change “cash card” to “credit card.” Let’s take a look at figure 3 below.

Observe that instead of transferring $200 a week onto a cash card (or simply taking out cash), you use a credit card that has a budget that you work against. Figure 3 also shows two formulas that help you manage your credit card usage within that budget.

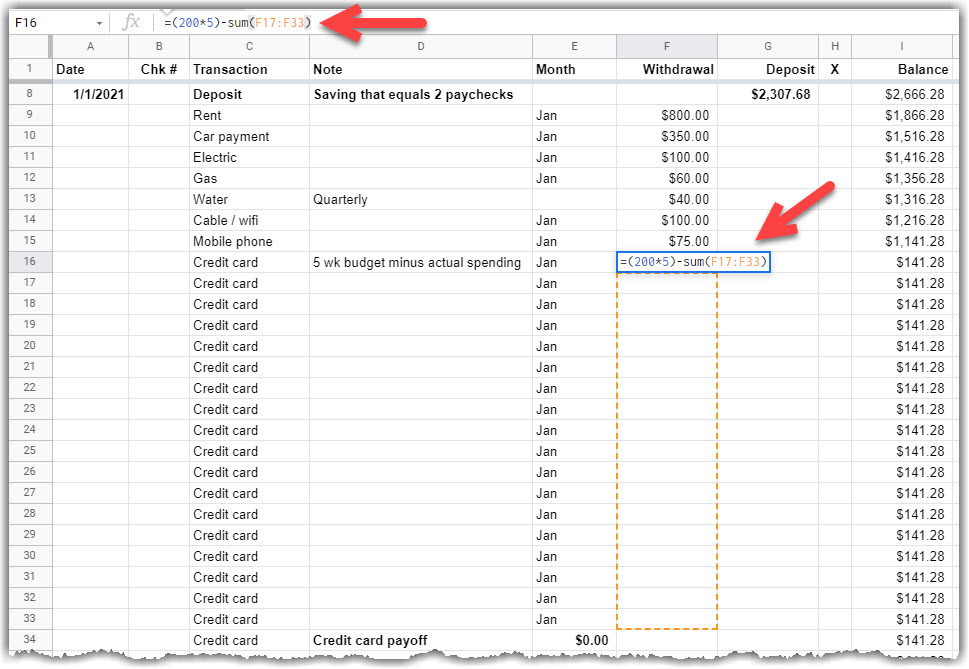

Formula 1: Five-week Budget minus Actual Spending

The purpose of a digital tracker and planner is to not only track actual spending, like you do with a paper check register. It’s about forecasting your spending and knowing if you buy that little something extra that you can still pay rent two months later. Therefore, it’s important to maintain your cash budget in the tracker. Formula 1 does that.

Below are the steps for setting up the credit card budget.

- Change “Cash card” to “Credit card”. If you want to use the card’s name, that’s fine.

- Delete the Notes. In our example, the note column reminds you that the $200 cash card is for food, gas, and miscellaneous. The notes will be replaced with actual purchase descriptions.

- Determine your cash budget. In this example, January has five Sundays so five weeks of cash: $200 a week.

- Insert a bunch of rows below the budget row. Don’t worry about adding too many or not enough. You can add and delete rows.

- Set up the formula. In this example, figure 4 shows the formula as =(200*5)-sum(F17:F33). Translated, that means, five weeks of $200 minus the cells that will hold your actual spending.

- Observe. The running balance remains at $141.28 as the five weeks of food/gas/misc. budget is still there, just in one row, not five.

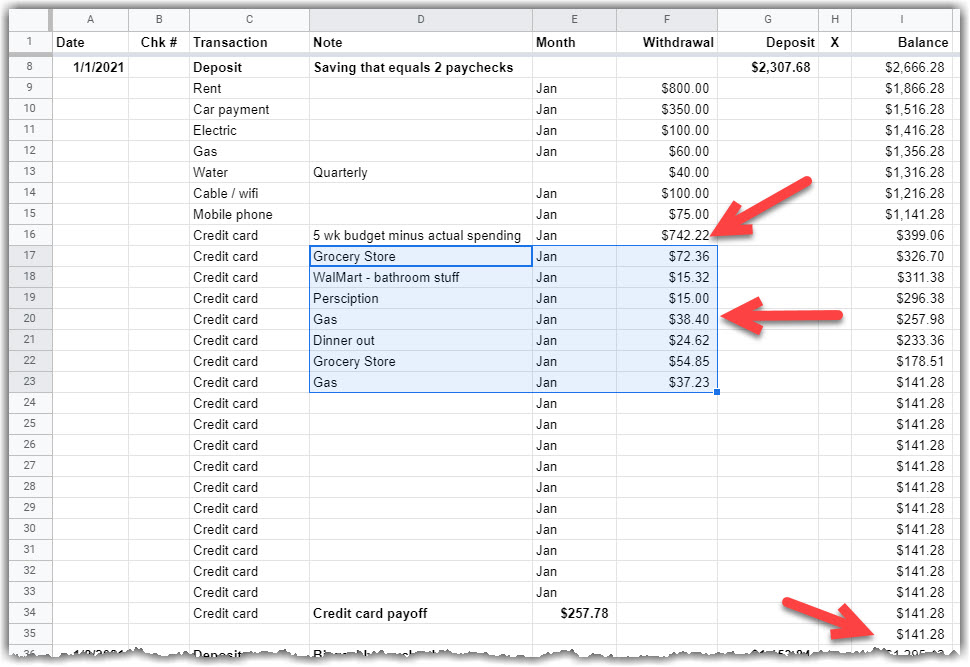

- Insert some test purchases. In this example, figure 5 below shows the addition of some food, gas, and other expenses.

- Observe.

- The $1,000 budget is now $742.22.

- The running balanced remains $141.28.

Formula 2: Credit Card Payoff Amount

When your credit card bill comes due, probably in the next month, you have the money set aside in your checking account to pay it. Therefore, you need a formula to keep track of the credit card payoff for the month.

This payoff formula shows what your credit card balance should show, assuming

- You have recorded all credit card transactions on the same card.

- The credit card had a $0 balance to start.

If that last assumption isn’t the case, you could insert a place holder for the amount you would have paid before using the credit card instead of the cash card. Let’s take a look.

- Insert the credit card payment formula. Figure 6 below shows the formula as =sum(F17:F33). That is the sum of all the purchases recorded.

- Observe.

- The formula is in the Month column. This is important. If you put the formula in the Withdrawal column, you will double count your purchases and the running balance would change inappropriately.

- The sum range is the same used in the first formula.

- The payoff equals the total purchases made to date.

- Include a minimum payment for previous balance. Figure 7 below shows $75.00 for a minimum credit card balance payment. It’s being paid using the $1,000 budget.

- Observe.

- The front loaded example used so far does not show a credit card payment planned. The assumption is, for this example, the previous balance being paid is for a recent large purchase: maybe tuition or a medical bill.

- The minimum payment for the previous balance reduces your five-week budget. Can you live within the budget reduction of $75.00?

- The credit card payoff is not an actual payoff. Think of it as a payoff of January’s purchases and a paydown of the previous balance. Interest will accrue on the previous balance but not January’s.

Large Credit Card Purchases

In the Financial Headaches: A Series on Personal Finance Management, credit card payments were not included in the examples. Instead, the use of the a credit card was provided as an option to pay tuition, a $685.00 bill that would exceed the funds available in January. Using a credit card means setting up a regular payment plan that will quickly pay off the balance.

Let’s look at how to do that by first looking at February before the credit card conversion in figure 8.

We need to change the cash card strategy to a credit card strategy. That means

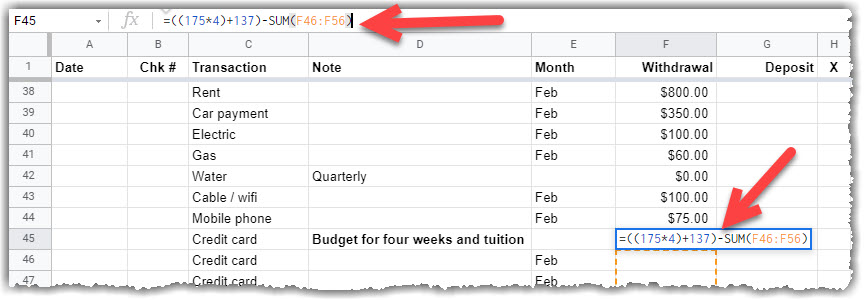

- The cash budget needs to be computed: four weeks at $175.00 a week. We’re cutting back due to school.

- Increase the cash budget by the tuition installment of $137.00. At some point, this amount will need to be adjusted to accommodate interest. Or, a 6th payment will need to be added to the plan.

What does February look like now?

- First the formula. Figure 9 shows =((175*4)+137)-SUM(F46:F56). Translated, that’s four weeks at $175.00 plus the existing budget for the tuition installment. Then, the sum of all the rows that will hold credit card transactions, just like January.

- Include the tuition paydown, just like figure 7 above showed a previous credit card balance minimum payment.

- Observe figure 10.

- Credit card budget for four weeks less the $137.00 tuition installment already entered as a purchase.

- Just like the January example, the credit card payoff amount is actually a payoff for all of February plus a paydown of the previous balance – in this scenario: tuition.

The Nature of Credit Cards

So far, we’ve been talking about using a credit card without ensuring you understand them. If you are new to the credit card world, let me fill you in on a few important details that you need to understand before you commit to this plan.

- When interest is charged – Most cards charge interest if you do NOT payoff the balance when it is due. So, read the fine print to ensure that interest starts being computed after the end of the month, not after each purchase.

- The interest rate. The range I have seen is 14% to 24%. This isn’t an issue if you don’t carry a balance.

- Each month that carries a balance will accrue interest. The balance equals purchases and previous interest.

- Paying interest on interest at 14% to 24% is something to something to avoid.

- Annual fees. Some credit cards charge annual fees. Avoid those. You don’t have to pay credit card companies the opportunity for them to charge you interest. Of course, if you need benefits such as purchase and travel protection, you might need a card that charges a fee. Read carefully. Some cards offer protection without a fee.

- Cash back. Some credit cards offer cash back. That money adds up.

“My first experience, back in the early 1990s, with a cash back credit card was when I received a paper ‘check’ in the mail that could be used at one of several stores. I was shocked and pleased. They came in $10 increments. And they were for stores where I shopped. I learned very quickly that charging everything and paying it off each month was a way to make money.”

me, the creator of the digital tracker and planner

The World of Credit Cards Giving Back

You can’t turn on the television without seeing a commercial for a credit card that will earn you miles or cash back or some other gift. It’s up to you to choose the benefit you prefer.

For me, the goal is to maximize my cash back and accumulated a nice bucket of money to pay for the holidays or a large purchase. To me, it’s free money.

To maximize cash back, you need to spend more. However, spending what you can’t pay off is a bad thing. So, what can you put on the card and payoff each month?

- Utilities bills – Make sure they don’t charge a fee for this opportunity. The cost can wipe out your cash back benefits.

- Internet/cable/phones – I used to pay my communication bill with my credit card. Then the provider offered me a $10 discount each month not to use my credit card. I did the math. The $10 discount was more than I could earn in cash back points.

- Small purchases – My parents would use cash for small purchases when they could have used a credit card and earned cash back. I taught them otherwise. Even vending machines take credit cards now-a-days.

Remember, every purchase, every charge needs to be recorded in your tracker. And, you have to stop charging when the tracker shows you have run out of money to pay off the balance of the credit card.

Closing thoughts …

This technique is not for the undisciplined. I have practiced this technique for decades and made about $1,000 a year. Spread over a year, that isn’t much per month. However, if someone handed you a check once a year for $1,000, would you say, “No thanks.” Of course you wouldn’t. Eye roll please.

To make this much back, I have to charge a lot. The years with big medical expenses have earned more than $1,000. But, you can also push up your cash back with higher percentage returns and no costs. I use credit cards that

- Provide 1% to 5% back on purchases

- Do not cap cash back each month

- Do not charge annual fees.

Good credit card habits can lead to higher credit scores. Good luck with your endeavors to manage your personal finances.

3 thoughts on “Credit Cards Can Make You Money and Raise Your Credit Score”