If you are just joining us, we are near the end of the series on personal finance management. This is the part where you reconcile the balance shown in your digital tracker and planner with the balance the bank shows.

The process used for this task has been around for … well, for as long as there have been bank accounts? Continuing with the plan set up in Lesson 5d, let’s jump in with the following steps.

- Copy all transactions reported by the bank that are not already included in the tracker. This step was explained in Lesson 6: Tracking Actual Commitments.

- Update the balance formula if you haven’t already.

- Click in the cell next to the balance of the last confirmed transaction. In other words, the last row with an X.

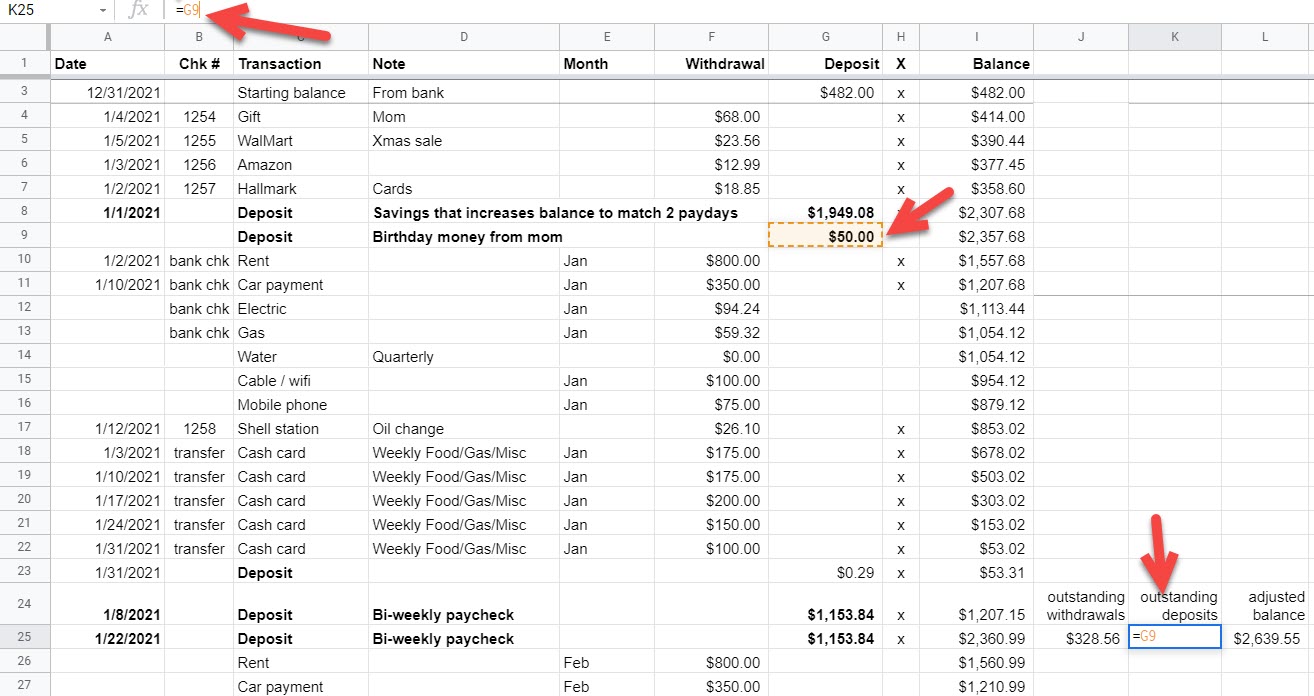

- Observe figure 2 below and the three numbers being calculated in columns J through L.

- Calculate the outstanding withdrawals. The formula in this example is =F15+F14+F12+F11. This formula adds the Withdrawals that have not cleared the bank.

- Calculate the outstanding deposits. The formula for this example is =G9. That is the one deposit that hasn’t cleared the bank, as shown in figure 3.

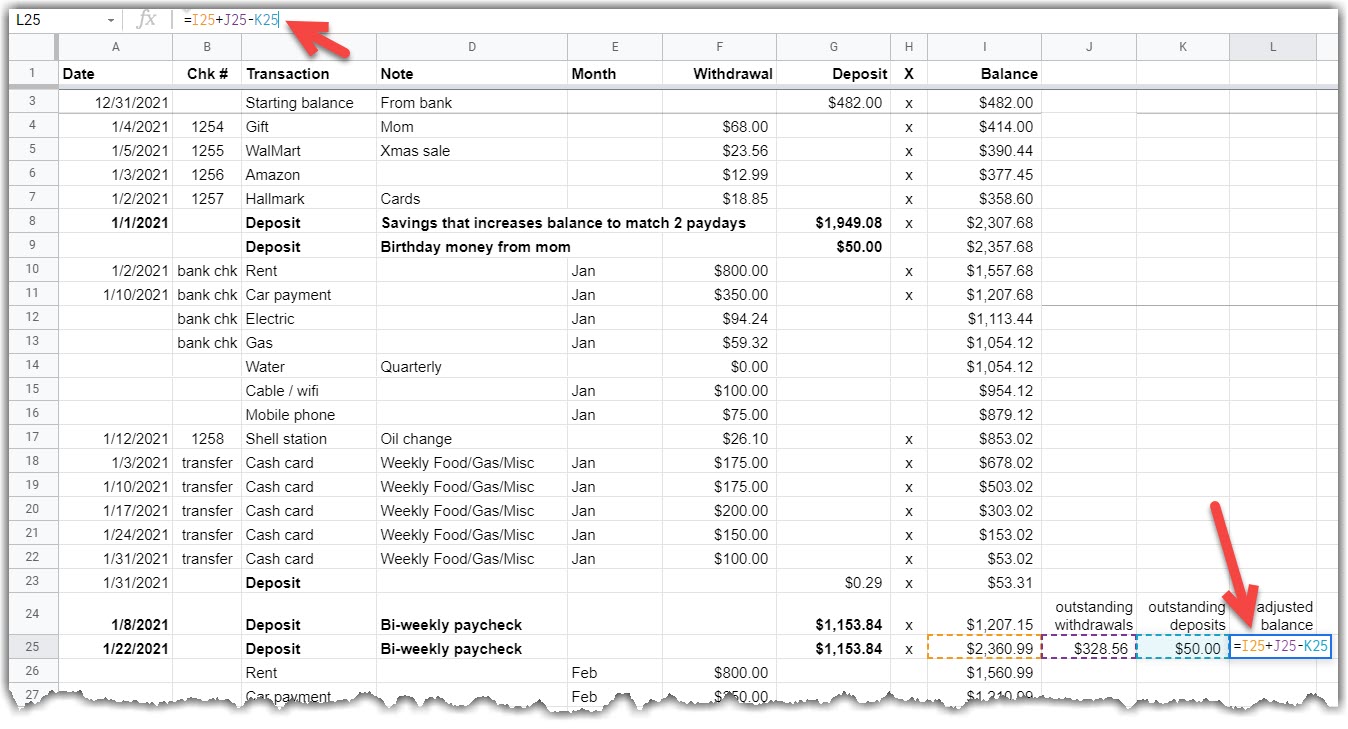

- Calculate the adjusted balance. The formula is always the same for this calculation: current balance plus outstanding withdrawals minus outstanding deposits. In this example, the formula looks like this: =I25+J25-K25 and is shown in figure 4.

- Obtain the bank’s ending balance as suggested in figure 5: $2,639.55.

- Compare your tracker’s adjusted balance with the bank’s ending balance. Figure 6 shows a zero difference.

“To this day, I hold my breath each time I compare my adjusted balance with the ending balance the bank reports. If I balance my tracker against the bank and the difference is $0.0, I sigh in relief.”

me, the creator of this series

When Your Tracker Doesn’t Reconcile

There are several reasons why this might happen.

- Typo in the tracker.

- Missing transaction in the tracker – withdrawal or deposit.

- Error in the formulas used to compute the tracker’s adjusted balance (e.g., you forgot about a check or deposit from months ago that hasn’t cleared).

“I have, in the past, waited up to three months to balance my tracker against the bank’s balance. My bad. The greater the number of transactions that need to be reviewed and verified, the greater the chance an error when reconciling. It’s a lot easier to balance frequently.”

me, the creator of this series

Next Lesson …

Has the running balance changed with the recent transactions? Lesson 8. Adjusting for the Future is the last basic lesson in this series.

5 thoughts on “Lesson 7. Balancing Against the Bank”