Let’s start by explaining what I mean by front loaded. The concept is simple. The income from one month is used to pay the next months commitments. Instead of talking about it, consider a sample using the income and commitments from Lesson 5c: Every Two Weeks Paycheck Plan.

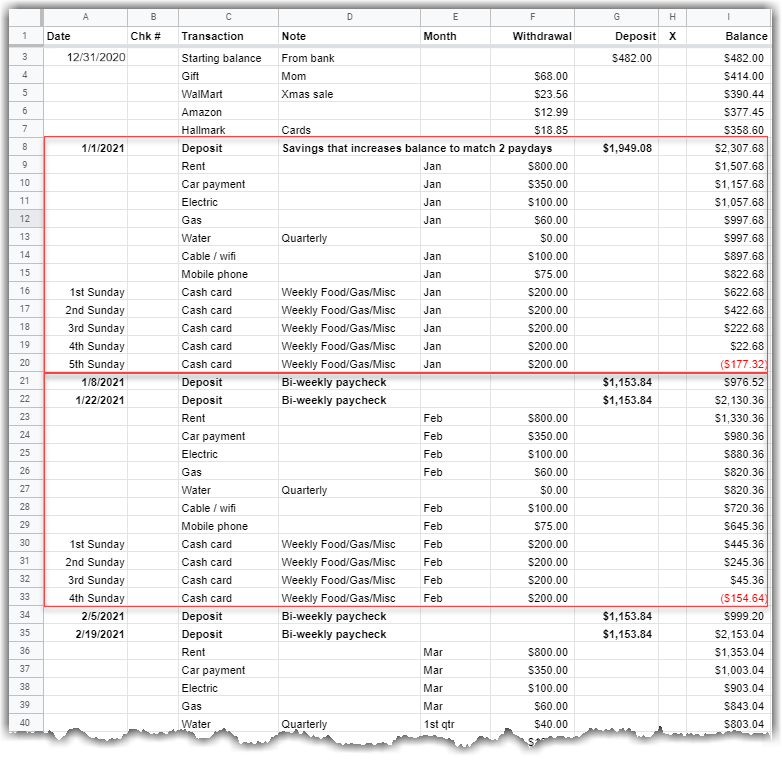

Sample Front Loaded Digital Tracker and Planner

Figure 2 illustrates a mix of concepts that you need to understand when using this approach.

- Kickstart the front loaded balance

- Incurred dates versus due dates

- Commitments versus Income

- Two versus three paychecks

- Negative tracker balance versus negative bank balance

Before you proceed with the topics below, please understand that the process described assumes you have experience managing your personal finances and practiced at least one of the following lessons.

- Lesson 5a: Single Monthly Paycheck Plan

- Lesson 5b: Twice a Month Paycheck Plan

- Lesson 5c: Every Two Weeks Paycheck Plan

Kickstart the Front Loaded Balance

In order to start the front loaded approach, your checking account needs a balance equal to that of one month’s income. In the scenario of a bi-weekly paycheck, that’s two deposits. There are multiple ways to achieve the initial front loaded balance.

- Current Balance – If the balance of your checking account equals one month’s worth of income AND there are no outstanding commitments that will lower that amount, you can start the process now.

- Savings – Use savings to increase your balance. Two options:

- Option 1 – Transfer the full amount. In this scenario, transfer: $1,153.84 X 2 = $2,307.68

- Option 2 – Transfer enough to bring the balance up to $2,307.68. In this scenario, transfer: $2,307.68 – $358.60 = $1,949.08. Figure 2 illustrates this scenario.

- Wait and Accumulate – It is possible, that over time, you can accumulate a balance in your checking account that will allow you to switch from a chronological approach to a front loaded approach without a contribution from your savings. The digital tracker and planner can give you a view into which month would be best to make the transition.

Incurred Dates versus Due Dates

Some bills represent commitments that have already been incurred and some represent future costs. For example, an electric bill paid in April might be for electricity used in March. However, a cable bill sent to you in April might be for services in May.

“I moved five times in a period of a few years. I learned very quickly that bills keep arriving after you turn off services. I converted my front loaded plan to represent commitments incurred versus the commitment pay/due date. It made for a more honest income-to-commitment connection. It also helped me ensure that enough money was kept in my account to cover the lagging bills.”

me, the creator of this series

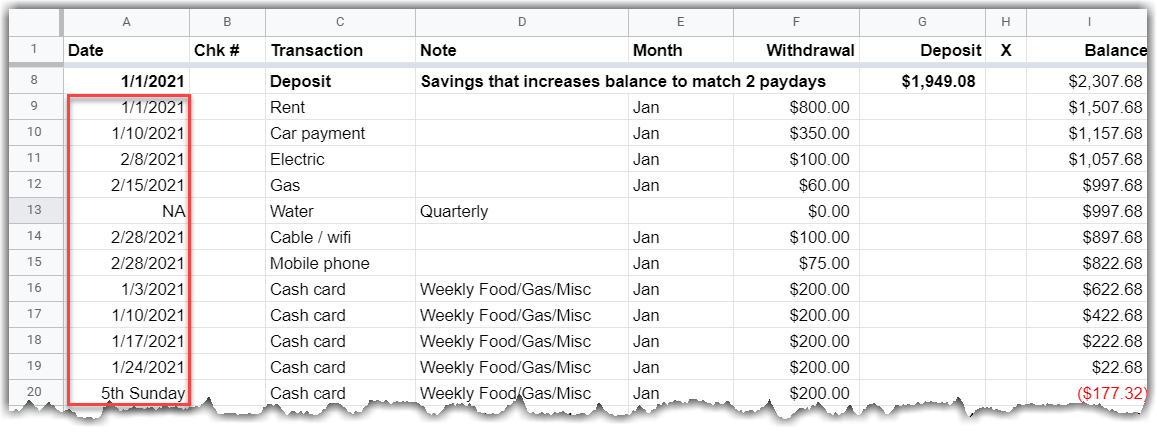

It’s up to you if you want to use incurred dates versus due dates. Figure 3 illustrates using an incurred approach.

Observe the following about figure 3.

- Multiple Months – A mix of January dates and February dates are included in the date column. The dates represent when the payment cleared the bank. The new Month column shows which month the costs were incurred. The idea of entering dates for when a check clears is a sneak peek into Lesson 6: Tracking Actual Commitments.

- Non-chronological – The dates are not in chronological order. For instance, the weekly cash withdrawals are compiled at the end of the list. This is a sneak peek into the a strategy explained in Credit Cards Can Make You Money and Raise Your Credit Score.

Commitments Versus Income

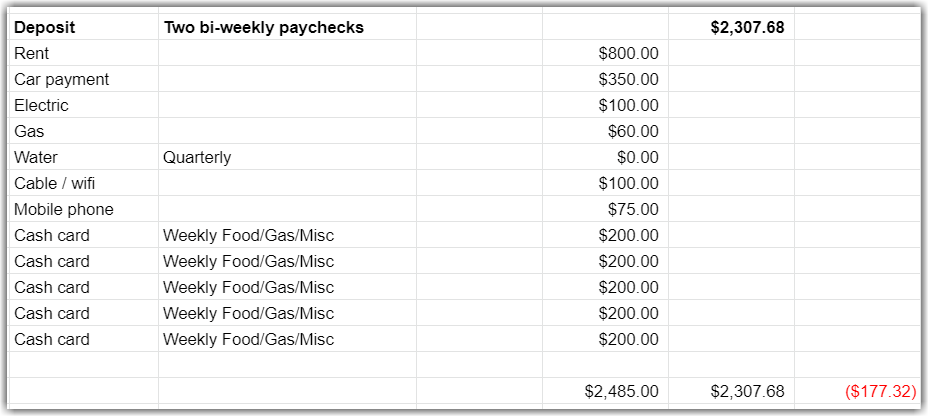

Depending on the month, commitments might exceed the two bi-weekly checks received in 10 of 12 months out of the year, as illustrated in figure 4 with the negative $177.32. Let’s look at what is happening in this example.

- Five Sundays – January has five Sundays which means five weekly Food/Gas/Misc. allotments. A month with only four Sundays would have a positive balance as removing $200 from the list of commitments offsets the negative $177.32.

- Quarterly Commitments – March includes a $40 water commitment for water used January through March. This creates a $17.32 overage in that month.

- Annual and semi-annual commitments – Tuition and taxes are two examples that will trigger a negative balance.

When faced with an income shortfall, there are options: some are more preferred than others.

- Preferred options

- Cut back – Don’t spend the $200 each week for Food/Gas/Misc. Clip coupons. Buy generic. Wait until you have the money. Immediate gratification can lead to financial problems.

- School loan – This big bill is unusual and might be the contributing to the negative balance. Consider applying for installment payments through the semester. That allows you to pay what you can each month.

- Potentially dangerous options – Borrowing for day-to-day living, be it via a credit card or from your own savings, creates unwanted debt that can snowball out of control and/or depletes savings meant for more urgent matters.

- Credit card – If you need a credit card to eat, you aren’t living within your means. However, your semester bill might be paid this way if a low-rate school loan is not available.

- Savings – Assuming you have a savings, what was it intended to support?

- School? – Okay. This makes sense for the tuition bill. Insert a row in the digital tracker and planner for the $685.00 deposit. That will offset the check for your tuition payment.

- Emergency? – Emergencies refer to scenarios such as large medical expenses or the loss of a job. Spend this account and you leave yourself vulnerable.

Two versus three paychecks

“I learned to live on two bi-weekly checks a month. Then, when the third check arrived, I socked it away for a rainy day.”

me, the creator of this series

For many in this situation, the third check is actually delayed income that is needed sooner than later. Using the digital tracker and planner, you can project months ahead to determine how long the positive balance from the third check will last.

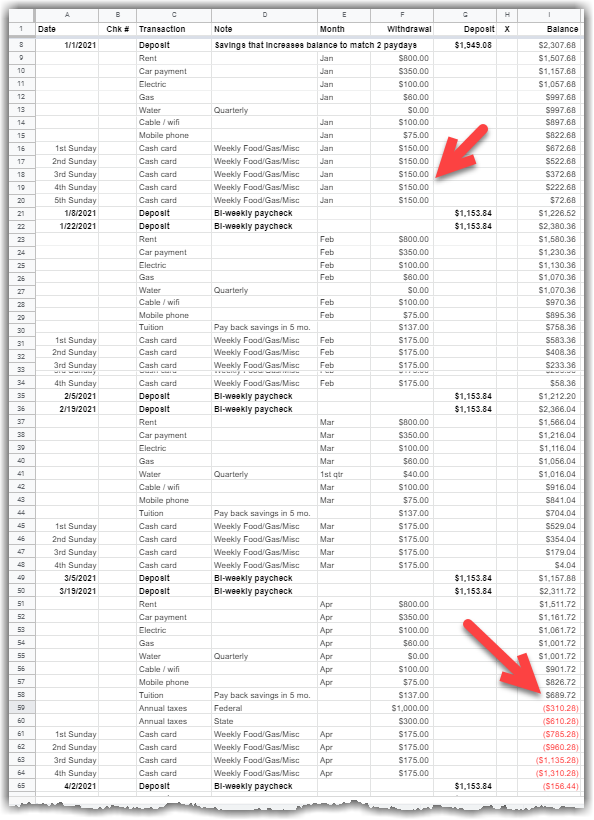

Negative Tracker Balance versus Negative Bank Balance

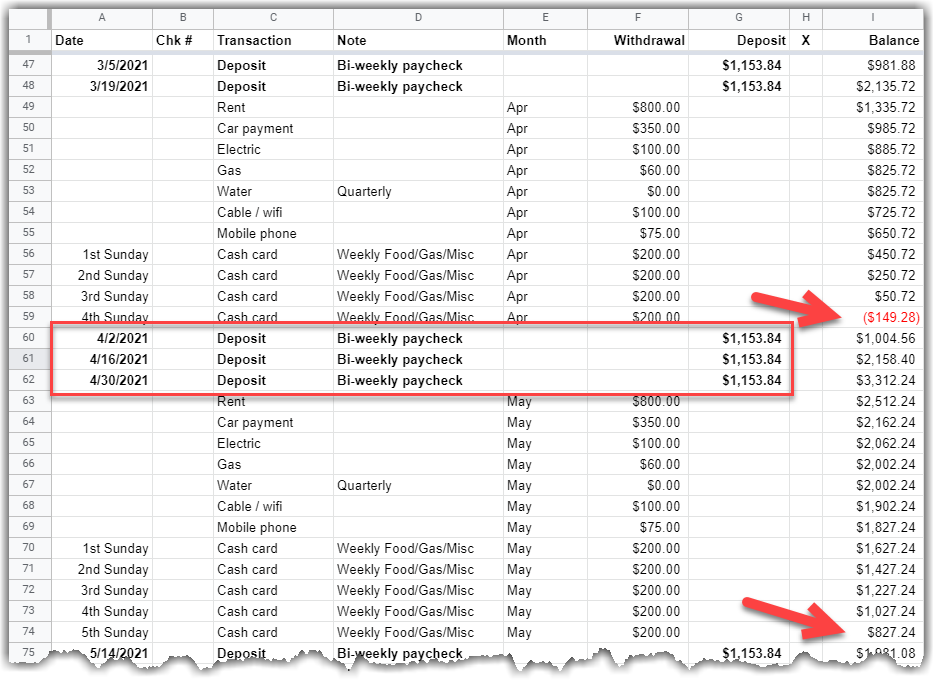

This concept is where the front loaded approach gets tricky. Technically, if the tracker balance goes into the red at the end of a commitment period (e.g., end of April in figure 5), the bank will likely show a positive balance. Why?

In this scenario, by the time the tracker balance goes negative, at least two paychecks will have been deposited in anticipation of May’s commitments. Although the bank won’t know about this negative balance, you are creating an issue by borrowing against the next month.

Tweak the Plan

Like the plans presented in lessons 5a, 5b, and 5c, the front load plan can project negative balances. Even if the front loaded approach shields you from the bank seeing the small negative balance, it still shows that the commitments for the month exceed the income. That means commitments have to be lower until income can be increased.

The tweaked plan in figure 6 implements the following to bring the plan into the black until tax season.

- Addition of the missing tuition and annual taxes included in previous lessons.

- Reduce the allotment from $200 to $175, except in January where additional reduction is needed because there are five Sundays in the month.

- Set up a payment plan for tuition by taking $685.00 out of savings and sending it directly to the university. It also assumes a payback plan that spans five months starting in February.

- The redundant water bill seen in the other plans has already been addressed in the sample.

- An estimate for annual taxes shows that some planning will be needed if taxes are owed.

Summary

The front loaded approach to the digital tracker and planner requires you to think outside the “check register” box. There are pros and cons to this approach.

- Pros

- It helps when the amount of one or more commitments exceeds the amount of one paycheck.

- It helps you manage costs as they are incurred versus when they are due, giving you the opportunity to manage future changes.

- Con

- In simple terms, some find the the non-chronological dates to be confusing.

“When I was just starting out, I bought an inexpensive condo with a small condo fee. I also had a car payment and credit card debt. Peanut butter and jelly sandwiches were a common meal. The mortgage payment exceeded the amount I received in one bi-weekly paycheck. The front loaded approach became the best approach for me.”

me, the creator of this series

Next Lesson …

Projected commitments aren’t necessarily real numbers. Therefore, you need to compare what you have to what the bank has. If you have been updating your tracker as you pay your bills, this step is a formality. At a minimum, Lesson 6: Tracking Actual Commitments confirms when checks have cleared.

12 thoughts on “Lesson 5d: Front Loaded Paycheck Plan”