At the end of Lesson 7, Balancing Against the Bank, the front loaded plan was balanced against the bank and the January withdrawals do not exceed the income assigned to that month, even with the $50 gift.

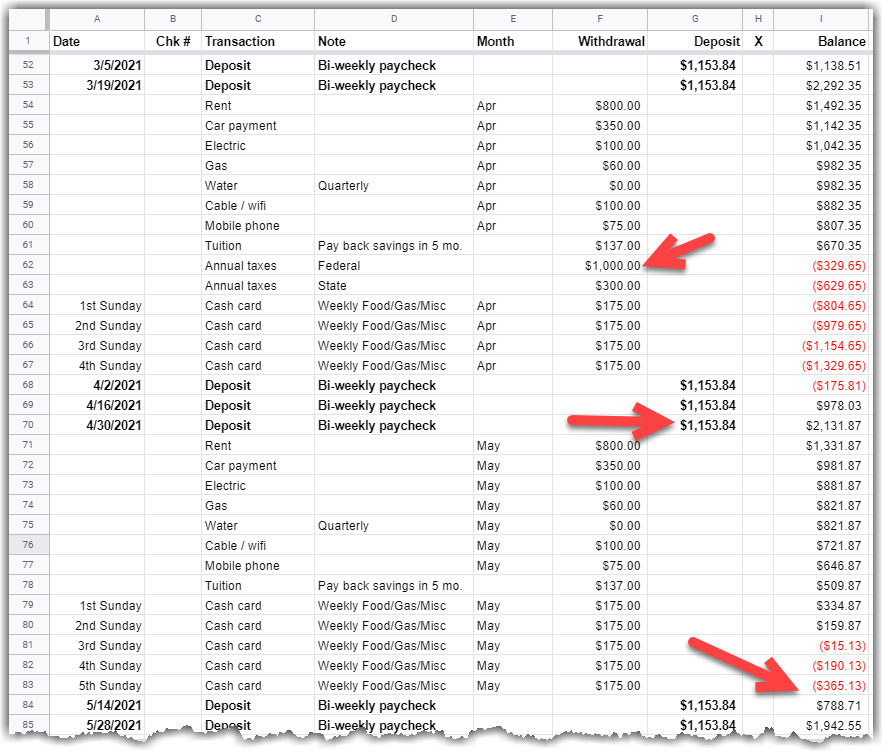

However, how does the future look? Scrolling down, the first negative balance appears in the month of April. An estimate of taxes owed based on the previous years taxes shows a problem on the horizon, as shown in figure 3.

With two months to plan, there are a few options. The question is, is it doable. Can you live on $150 a week? Figure 4 below shows how reducing weekly spending from $175 to $150 through May can make a difference. But, that’s not all.

April has three paychecks. The first arrives very close to the end of March: Apr 2nd. Assign that first paycheck in April to the front load checks for April’s commitments and watch the red go away. The balance after the estimated taxes are paid is projected to be $124.19. And, May’s ending balance is also in the black with $59.87.

What if you increased your income?

So far, our example has created a tight budget situation, something many people experience. Increasing income, obviously, is one way to address living paycheck to paycheck.

“Covid 19 hit and I lost my job. I took a job that didn’t guarantee a minimum paycheck because it was using a skill set that wasn’t a valuable. After working with Cindy, I realized that the lack of regular income was creating problems I hadn’t considered. So, I got a job using skills that pay more. With the increase, my wife and I are back on track.”

annonymous client

A raise, more hours, or a new job isn’t always an option. For a short time, while you get your financing under control, the following might be an option.

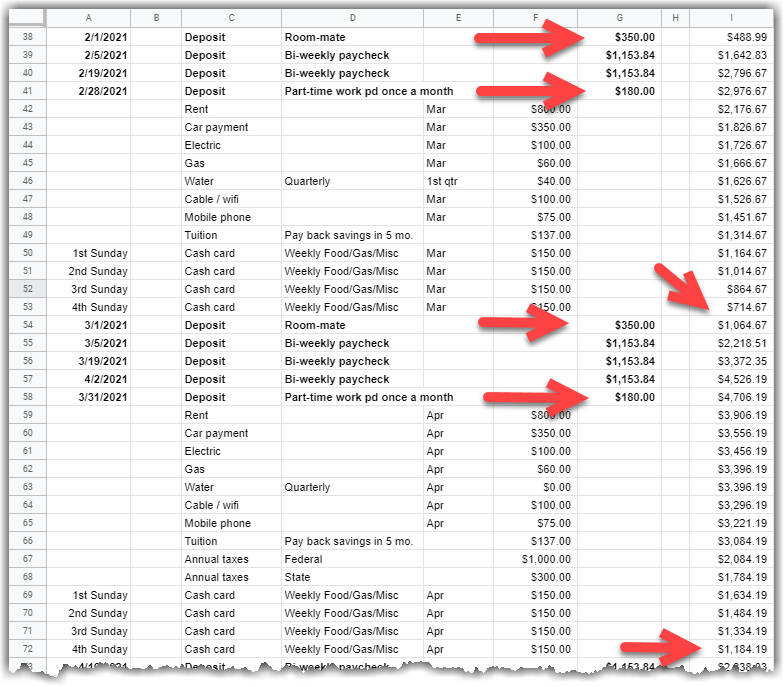

- Rent out a room. Roommates aren’t always fun, but it’s not forever.

- Take on a part-time job. We aren’t talking high-pay work. Working weekends for minimum wage can bring in a few extra dollars that add up.

Let’s look at what happens to the front load plan with these two options.

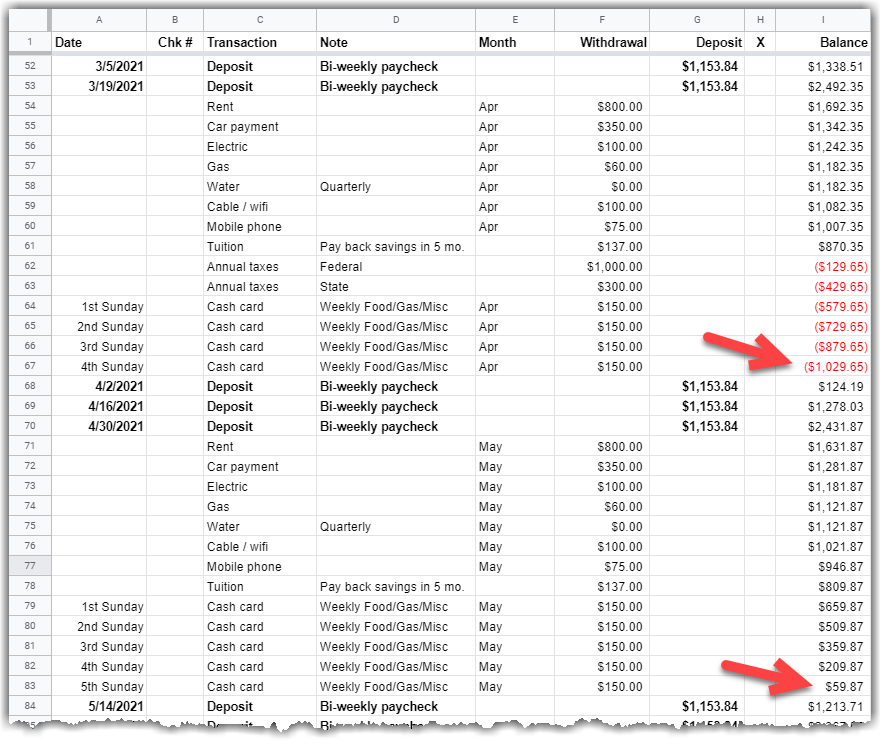

Figure 6 shows April with an ending balance project to be $1,184.19. Before the extra income, figure 5 showed the projected balance at $124.19.

Would you go on a spending spree with the extra money? Or do you see how much you have to sacrifice to make the extra income and therefore, you’ll save it. Or maybe you will payoff a credit card and start saving the fees credit cards charge.

“I set up my tracker so that the line below by paycheck deposit was a transfer to my savings. Sometimes it wasn’t much and other times it was a lot. It helped that I didn’t see a big balance in my checking account. It kept me from spending when I don’t need to.”

29 year old learning a valuable lesson

Real Life

Recall from Lesson 3: Get Ready that there are fixed commitments and variable commitments. You saw in Lesson 6: Tracking Actual Commitments that utility bills can be different than planned. In this scenario, the actual costs came in lower than the plan. They could have come in higher.

You also saw that car maintenance was need and weekly spending varied. Lesson 3: Get Ready lists several potential commitments that can send your balance into the negative really fast.

A goal to stay with the plan is the first step in succeeding. The next goal is to find other ways to save, if not increase your income, as you saw in figure 6. Until you are not living paycheck to paycheck, you should monitor your digital tracker and planner very closely.

Next Up …

Plan. Practice. Change your behavior if the numbers tell you there are problems.

Get new content delivered directly to your inbox.

5 thoughts on “Lesson 8. Adjusting for the Future”