If you completed the tasks in Lesson 3: Get Ready and Lesson 4: Set Up the Spreadsheet, you are ready to move forward in preparing your digital tracker and planner. If you reviewed Lesson 5b: Twice a Month Paycheck Plan, you will not be surprised regarding the steps that follow. However, there is a difference so please continue.

In this lesson, you are going to focus on a scenario where you get one paycheck every two weeks (i.e., bi-weekly). After you complete this lesson, you might find that Front Loaded Paycheck Plan in Lesson 5d is beneficial as it is similar to a person who receives a paycheck at the start of each month.

Let’s get started with the following actions.

- Enter financial commitments and income

- Add actual starter data

- Update the balance calculations

- Tweak the plan

For comparison opportunities, this lesson uses the same income and expenses shown in Lesson 5a: Single Monthly Paycheck Plan and Lesson 5b: Twice a Month Paycheck Plan.

Enter Financial Commitments and Income

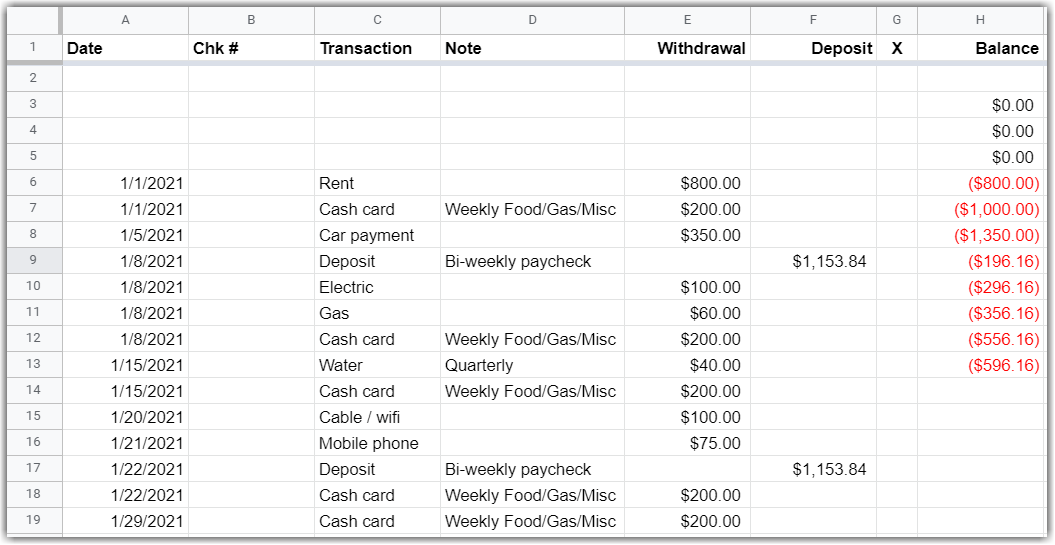

In Lesson 3: Get Ready you gathered the type of commitment, the anticipated amount, and the due dates. Add this information to the sheet for twelve months from your selected start date using the following instructions.

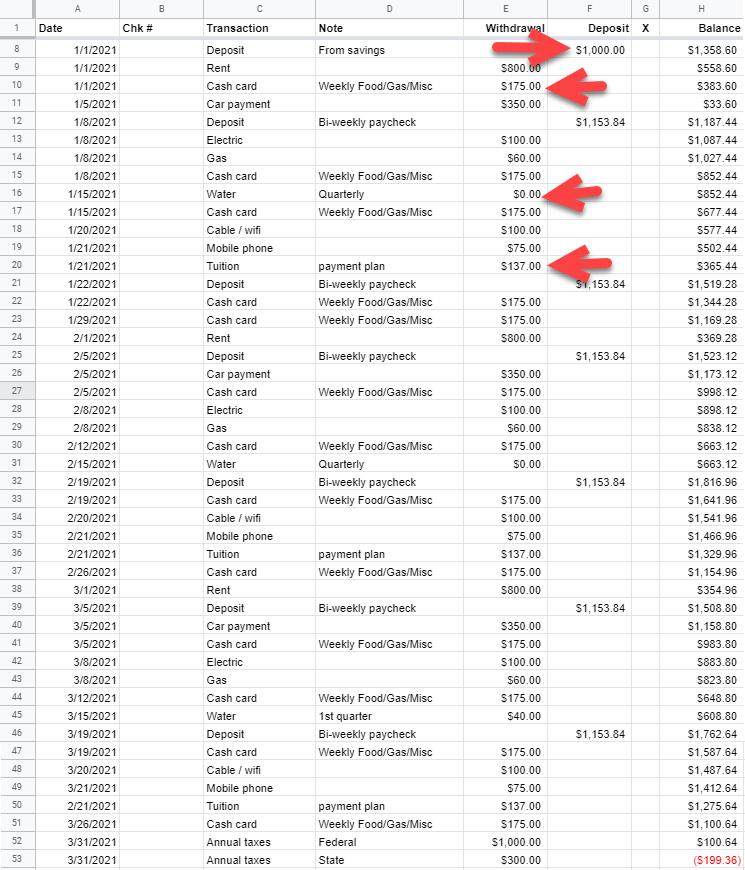

- Enter one month’s worth of information (as shown in figure 2 below), leaving a few lines at the top of the list for when you are ready to add the current balance and outstanding commitments not cashed. Don’t worry about leaving enough or too many. Rows can be inserted or deleted when you are ready.

- Copy and paste the month eleven times and change the dates accordingly.

- Insert rows for expenses that occur semi-annually or annually. For example, three commitments might be

- Tuition for your master’s degree.

- Annual tax bill because you suspect this year’s tax bill will likely be the same last year.

- Personal property taxes, but the screenshots don’t show it.

Add Actual Starter Data

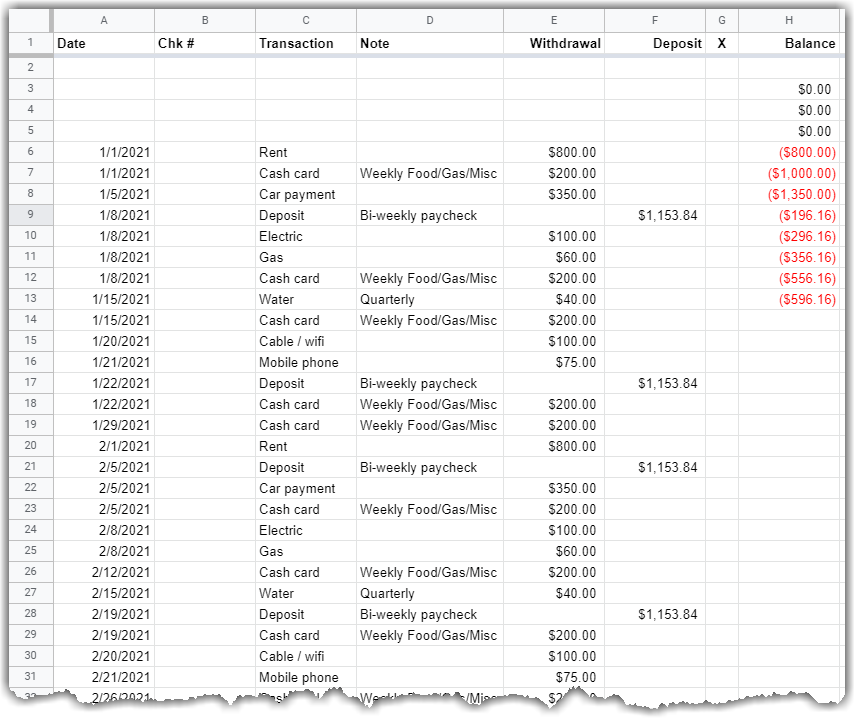

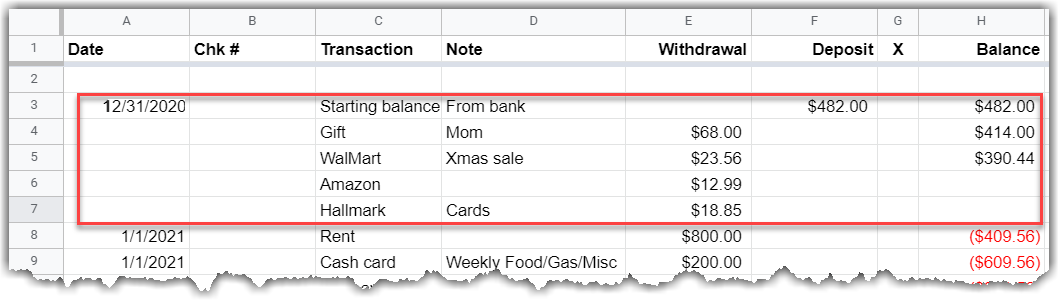

Now your digital tracker and planner is ready to receive actual versus planned data. If you need to add more rows, please do so. In the example below, the following have been added:

- Starting balance as a deposit. This is the current balance of your checking account. This is also the time when the digital tracker and planner replaces your paper check register.

- Outstanding commitments that you know have not cleared the bank as withdrawals. In this scenario, holiday related purchases.

- In this scenario, all of the December bills have been paid and processed by the bank.

Update the Balance Calculations

In this step, you will learn a very important aspect regarding sequenced formulas: patching. I just made up the term patching because I needed to call it something. However, you will see with the following mini-tutorial below makes that term descriptive.

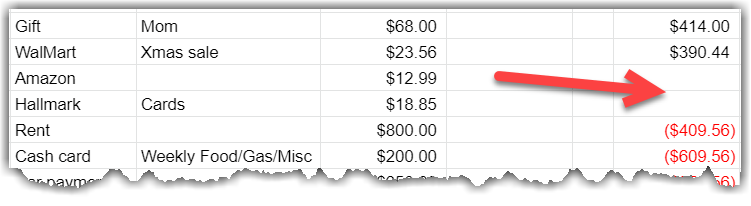

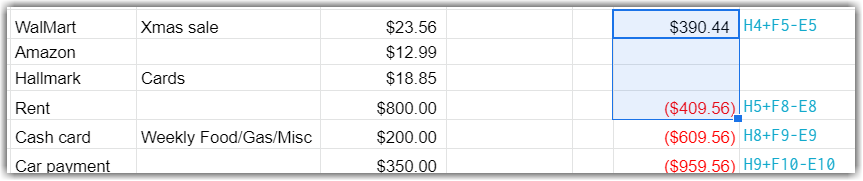

Observe the gap in the formulas caused by the Amazon and Hallmark purchases.

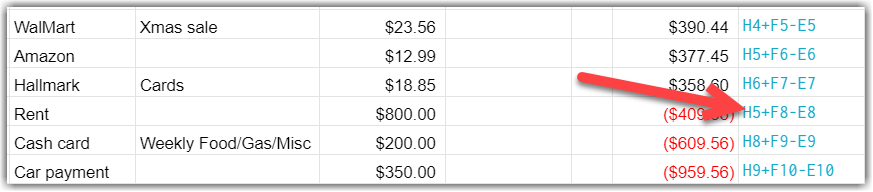

Incorrect Way to Patch the Gap

Your first thought might be to copy the formula from row 5 to the empty rows: 6 and 7. Let’s see why that won’t work. The image below shows the formulas from the balance column.

Notice the following:

- Formula inconsistency. The H value, how it goes from 4 to 5 to 6 to 5 to 8. The H value should always increase by 1, therefore the second 5 value is the problem.

- The balance doesn’t change. Line 8 before the formula insert is $xxxxxxx. Line 8 remains the same after copying the formula into the empty lines when it should decrease.

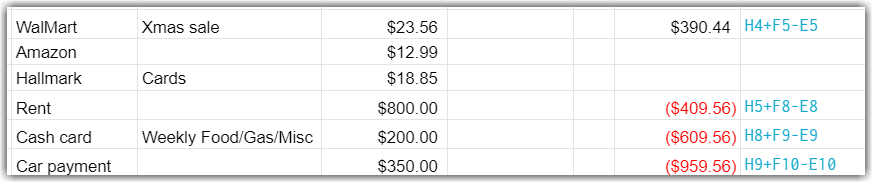

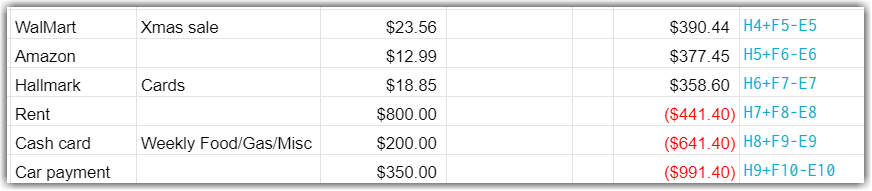

Correct Way to Patch the Gap

- Let’s delete the wrong formulas from rows 6 and 7 and start again.

- Stretch the highlight from the formula above to the formula below the gap.

- Click Ctrl+D on a PC or Command+D on a Mac to duplicate the formulas. I described this process recently as, “It’s like spreading peanut butter.” My client recommended I share that here.

- Observe the changes.

- The H value increases by 1 before and after the gap is patched.

- The balance decreases from ($406.56) to ($441.40) on row 8, accordingly.

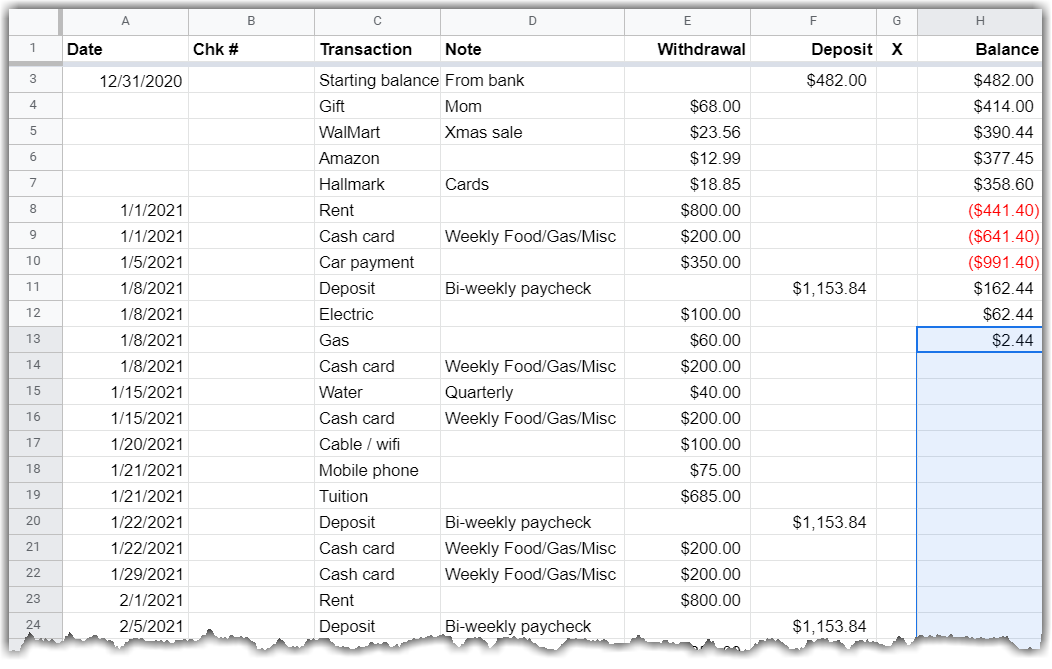

- Now, fill in the rest of the formulas. Highlight the last formula and the subsequent cells.

- Duplicate the formulas by clicking Ctrl+D on a PC and Command+D on a Mac.

- Observe what happened in this example. Did something similar happen to you?

- There will be a time when you don’t receive a paycheck at the start of a month.

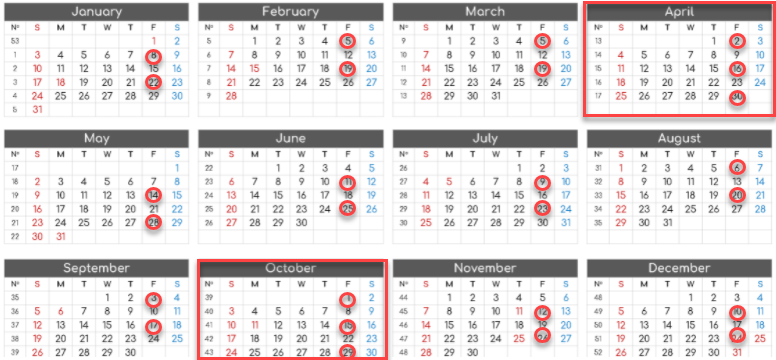

- In the previous lessons, the pay per month was the same: $2,500. In this instance, when the yearly pay is spread across 52 weeks, the amount is lower. However, it also means that there are two months that experience three deposits, as shown in figure 1 at the start of this lesson.

- The lagging expenses from December haven’t cleared the bank, but you are setting aside that money for when they do. It’s likely that you have those amounts in your paper check register so this isn’t anything new. However, I have found that not everyone is as diligent in keeping track.

- The starting balance adds funds to your tracker, but not enough to cover the commitments due at the start of the month.

- Even though timing and reduced check amounts play a role in creating the negative balance, there are still issues that need to be addressed.

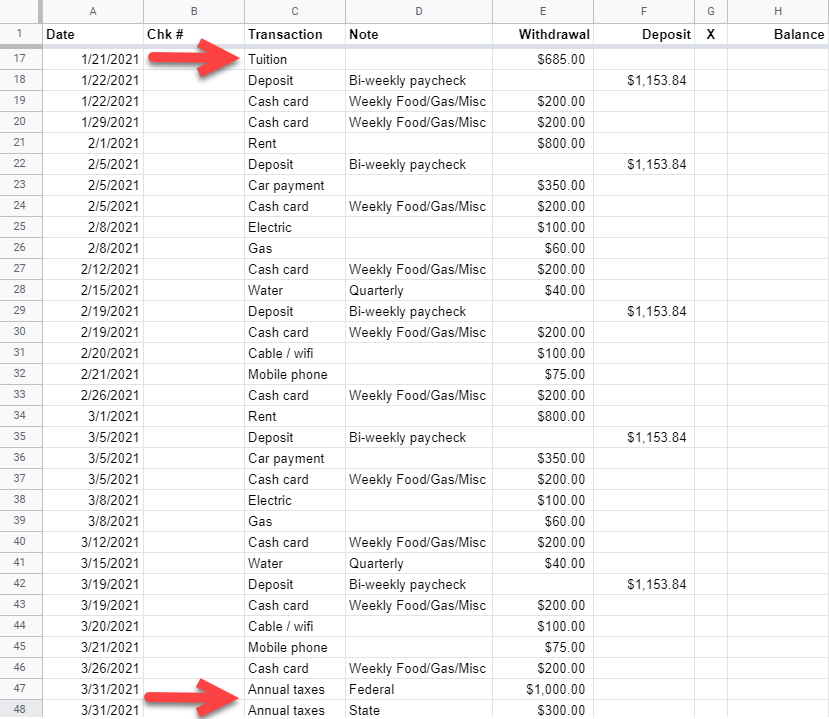

- The total income deposited in 10 of 12 months is less that total commitments.

- Minimum monthly income: $2,307.68

- Expected monthly commitments: $2,525.00

- Annual and semi-annual commitments only make paying your bills more difficult.

- The total income deposited in 10 of 12 months is less that total commitments.

- Consider addressing negative balance options

- Preferred options

- Cut back – Don’t spend the $200 each week for Food/Gas/Misc. Clip coupons. Buy generic. Wait until you have the money. Immediate gratification can lead to financial problems.

- School loan – This big bill is unusual and might be the contributing to the negative balance. Consider applying for installment payments through the semester. That allows you to pay what you can each month.

- Potentially dangerous options – Borrowing for day-to-day living, be it via a credit card or from your own savings, creates unwanted debt that can snowball out of control and/or depletes savings meant for more urgent matters.

- Credit card – If you need a credit card to eat, you aren’t living within your means. However, your semester bill might be paid this way if a low-rate school loan is not available.

- Savings – Assuming you have a savings, what was it intended to support?

- School? – Okay. This makes sense for the tuition bill. Insert a row in the digital tracker and planner for the $685.00 deposit. That will offset the check for your tuition payment.

- Emergency? – Emergencies refer to scenarios such as large medical expenses or the loss of a job. Spend this account and you leave yourself vulnerable.

- Preferred options

“I spent my paycheck on what I wanted when I wanted. Then, when my truck broke down, I couldn’t pay for the repair. So, I spent my inheritance on the repair instead of the house my grandparents hoped I would use it for.”

– anonymous

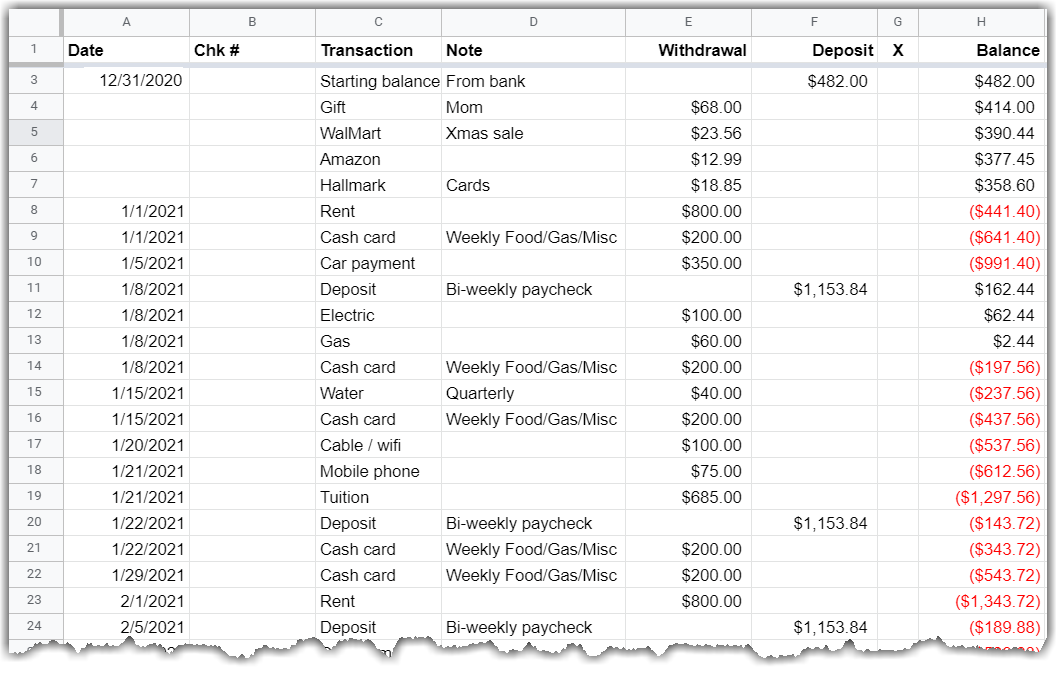

Tweak the Plan

Planning a negative balance is not a good plan, obviously. So, how can you turn the red into black?

Several adjustments were made to lower commitments and balance the plan up to tax season.

- Transfer $1,000 from savings. If you don’t have savings, this scenario demonstrates how spending your prior paycheck on the holidays can leave you without the necessary funds for your commitments. Your rent and car payment might be late.

- Correct a quarterly commitment recorded for each month: Water bill. That only happens every three months.

- Reduce the allotment from $200 to $175. It means brown bagging lunch and/or drinking the free office coffee. It could also mean not indulging in vaping or smoking, for instance.

- Obtain a student loan that breaks your tuition payment into five installments. If this doesn’t work, consider

- Using a credit card. There will be interest applied, but you might owe interest in the installment plan as well. Set up a five month payment plan to pay off the credit card.

- Using your savings. The same payment plan applies so you can pay yourself back and rebuild your savings.

- The negative balance anticipated near tax time is still an issue. When the time comes, this amount might be more or less. However, the same payment options apply.

- Return to the budget and see it you can live on $150 a week to lower the potential negative balance even further.

- Use a credit card that you payoff quickly.

- Borrow from yourself but payback savings quickly. Do not take money from your 401K. It’s a bad habit to start and it can be expensive as you will owe taxes on it.

Next Lesson …

Your next lesson depends on your specific situation. If your paycheck deposit matches this scenario

- But you are facing negative balance numbers, Lesson 5d: Front Loaded Paycheck Plan might help.

- And you like the way your balance is working, Lesson 6: Tracking Actual Commitments is the next step.

8 thoughts on “Lesson 5c: Every Two Weeks Paycheck Plan”